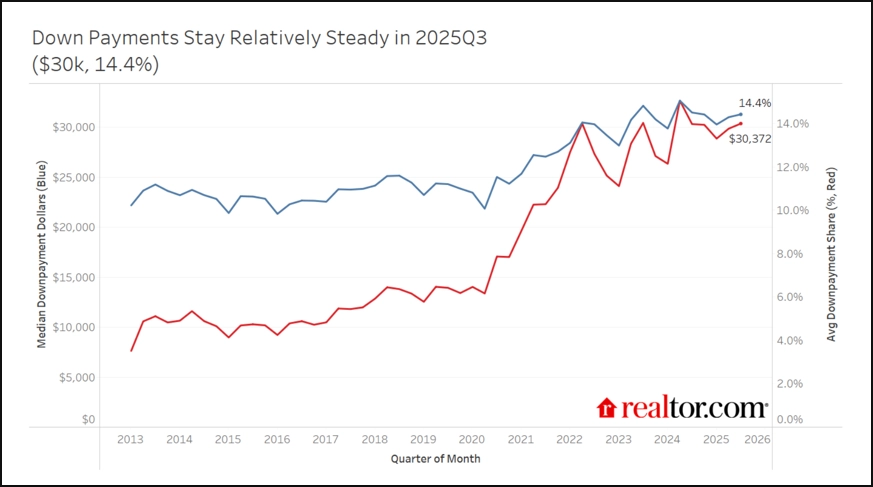

No, most homebuyers make a down payment that's well below 20%. Recent research suggests the typical down payment in 2025 was 14.4%.

The 20% down payment myth has been around since the Great Depression, but buyers today can get loans with much lower down payment requirements.

In this article, I'll explain more about down payment myths and realities.

The Harmful 20% Myth

Among the many myths that go along with buying a home, one of the most damaging is the idea that you need at least a 20% down payment. Surveys over the years have often shown that many buyers who could afford a home don't even try because they assume a 20% down payment is required.

In the Tri-Cities, with our current median sales price around $425,000, a 20% down payment would mean a minimum $85,000 out of pocket -- and that would lead a lot of buyers to give up on the dream of owning a home.

It's a myth that stops the homebuying process before it starts.

So, what down payment do you need to buy a house?

It depends on what kind of loan you're getting, according to The Mortgage Reports.

With a conventional loan, the minimum down payment is just 3%. With an FHA loan, the minimum is 3.5% as long as you have a credit score of 580 or above. (If your credit score is below that, FHA loans require a 10% down payment.)

Government-backed VA loans and USDA loans are even less stringent -- they can be had with a 0% down payment.

According to Realtor.com research, the average down payment was 14.4% in Q3 of 2025.

What does this mean for you?

If you're thinking about buying a home soon, keep in mind that you don't have to put the full 20% down.

If you're interested in learning more about down payment assistance programs, I can help you connect with a trusted lender who will work with you to figure out all of your options in the homebuying process.

If you want to purchase a home this year, let's connect to start the conversation and explore your options.

- Cari